Bank Accounts for Babies in Louisville, Kentucky

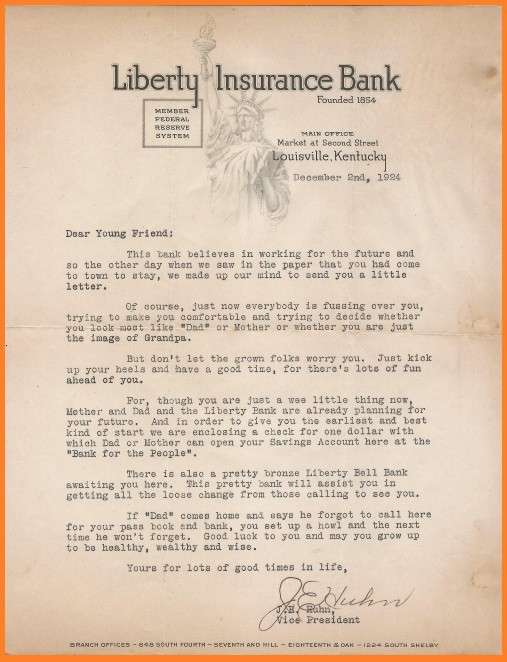

AT THE BEGINNING OF December 1924, John E. Huhn, Vice President of the Liberty Insurance Bank of Louisville, Kentucky, sent a solicitation letter under his signature to a three-week old newborn. The missive contained a greeting and a proposition. “Dear Young Friend”, the salutation began (for Huhn did not know the baby’s name) …... ”when we saw in the paper that you had come to town to stay, we made up our mind to send you a little letter ...… though you are just a wee little thing now, Mother and Dad and the Liberty Bank are already planning for your future. And in order to give you the earliest and best kind of start we are enclosing a check for one dollar with which Dad or Mother can open your Savings Account here at the ‘Bank for the People.’ “.

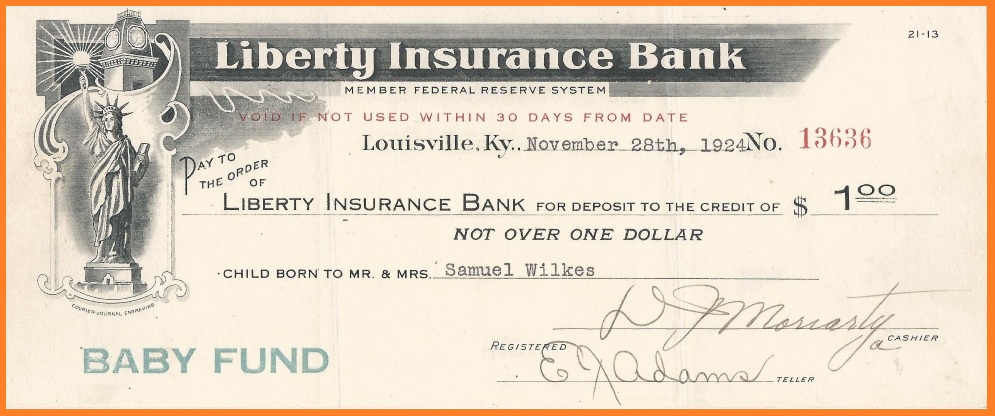

This promotional check, sent to Samuel and Sarah Wilkes, sought to encourage the parents to start a bank account for their newborn (Image source: author's collection).

The check, which was meant to be deposited to the credit of the “child born to Mr. and Mrs. Samuel Wilkes, was issued as part of a marketing program by the Liberty Insurance Bank to expand its already-considerable deposit base. Inaugurated in 1920, the “Bank Accounts for Babies” plan offered to each child born in Jefferson County, Kentucky, a one-dollar check with which their parents could start a savings account on their babies’ behalf. The parents of twins would receive five-dollar checks, while the lucky producers of triplets would garner fifteen dollars—money which would be theirs only if they opened up bank accounts for their newborns. Otherwise, as the checks advised, the offer would become void if the checks weren’t deposited within thirty days. To sweeten the deal, Huhn’s letter promised the new depositor “a pretty bronze Liberty Bell bank” into which the little tyke could stash whatever spare change came its way. These Liberty Bell banks, distributed around the country by the Bankers Saving and Credit System Company of Cleveland, Ohio, were a staple of bank marketing in the early 20th century. The idea was that accumulating coins in the toy bank would inculcate habits of thrift in the growing child, encouraging them to become depositors and customers of the bank when they reached adulthood. In the meantime, it was up to the parents to make the first move. As Huhn’s letter presumed to advise the newborn, “if ‘Dad’ comes home and says he forgot to call here for your pass book and bank, you set up a howl and the next time he won’t forget. Good luck to you and may you grow up to be healthy, wealthy, and wise. Yours for lots of good times in life, J. E. Huhn.”

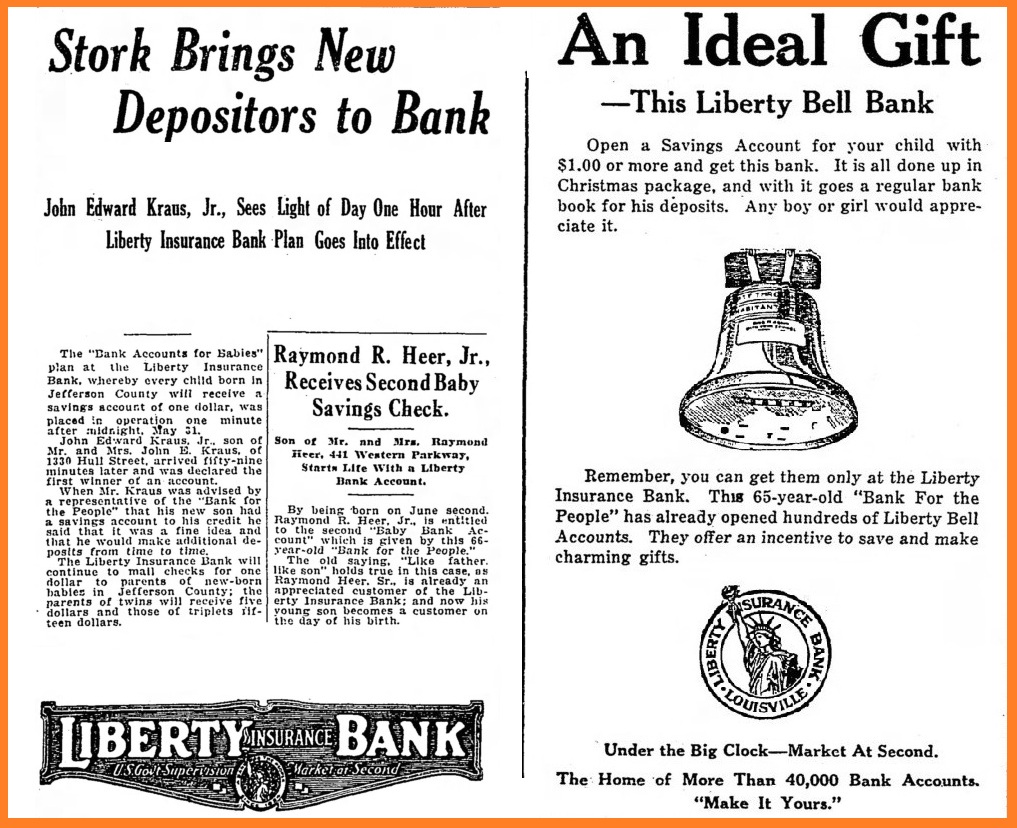

ABOVE: The solicitation letter, addressed to the Wilkes' newborn child, accompanying the $1.00 check. Starting in 1920, Liberty Insurance Bank sent similar offers to all children born in Jefferson County, Kentucky (Image source: author's collection). BELOW: Liberty Bank announces the first newborn customers under its Bank Accounts for Babies plan (L); the offer of Liberty Bell banks for children's deposits (R).

(Image sources: The Courier-Journal, Louisville, KY, June 17, 1920; December 14, 1919).

Liberty Insurance Bank, “the Bank for the People”

Bank Accounts for Babies was just one of a number of saving initiatives undertaken by an institution that, by the early 20th century, was the largest state-chartered bank in Kentucky, with a deposit base consisting of tens of thousands of small accounts drawn mostly from the Louisville area. The Liberty Insurance Bank began its own life in 1854, when it was granted a charter by the Kentucky state legislature as the German Insurance Company. Organized by local merchants of German descent (although its first President was of French background), the company was originally authorized to conduct both an insurance and a banking business. An 1872 law required the company to split into separate insurance and banking concerns, the result being the German Insurance Bank and the German Insurance Company. Connections between the two companies remained close: they shared the same Board of Directors and the insurance company kept its surplus on deposit at the banking company.

granted a charter by the Kentucky state legislature as the German Insurance Company. Organized by local merchants of German descent (although its first President was of French background), the company was originally authorized to conduct both an insurance and a banking business. An 1872 law required the company to split into separate insurance and banking concerns, the result being the German Insurance Bank and the German Insurance Company. Connections between the two companies remained close: they shared the same Board of Directors and the insurance company kept its surplus on deposit at the banking company.

Like many other commercial banks around the United States in the early 1900s, the German Insurance Bank made greater efforts to solicit the accounts of small savers to build its deposit base. During the 19th century, commercial banking had largely ignored small savers, leaving their interests to be served by specialized institutions that were either connected to mortgage lending or which had eleemosynary missions. This began to change as a swelling middle class generated financial surpluses that could be channeled into the banking system. Acknowledging the growing importance of saving, the American Bankers Association created a Savings Bank Division in 1902. In the competition for savings accounts, state-chartered banks had the advantage, as the laws under which they operated permitted more flexible ownership structures than national banks. Many state laws allowed commercial banks to operate savings departments or their own affiliated savings institutions before federal laws like the McFadden Act of 1927 explicitly authorized similar actions for national banks. Beginning with the Federal Reserve Act of 1913, which relaxed restrictions on real estate lending by national banks and permitted them to undertake a trust business, state and nationally-chartered institutions competed on a more equal footing.

As they chased small-dollar savings deposits through a variety of marketing appeals, banks participated in a larger social project to encourage the practice of thrift in the United States, an agenda with moral overtones that was promoted by social institutions and public authorities. World War I gave a great stimulus to this agenda thanks to the need to sell billions of dollars’ worth of War Savings Stamps, Liberty Bonds, and Victory Bonds to the American people, an experience that not only reinforced habits of thrift but democratized finance by introducing the general public to the idea of owning bonds, and to securities investments more generally.

The German Insurance Bank’s own efforts to expand its deposit base and promote habits of thrift were closely connected  with the career of John Ernest Huhn (1880-1968). Born in Germany, Huhn grew up in Louisville, attending high school there until he left to take a job as a runner (messenger) at the bank. Huhn rose quickly through the ranks and, when the bank decided to establish a savings department in 1913, he was made its manager. Huhn brought energy and resourcefulness to his new role, implementing promotional schemes that attracted the approving notice of national banking publications. Variations on the Bank Accounts for Babies idea were adopted by bank marketing around the country, often in the form of premium schemes whereby retail store customers earned certificates with different face values, corresponding to the amounts of their purchases, which local banks would then accept as if they were cash deposits into children’s accounts. In contrast, Huhn’s $1.00 checks seemed like a superior twist since they went stale after one month and thus wouldn’t create an overhang of liability for the bank.

with the career of John Ernest Huhn (1880-1968). Born in Germany, Huhn grew up in Louisville, attending high school there until he left to take a job as a runner (messenger) at the bank. Huhn rose quickly through the ranks and, when the bank decided to establish a savings department in 1913, he was made its manager. Huhn brought energy and resourcefulness to his new role, implementing promotional schemes that attracted the approving notice of national banking publications. Variations on the Bank Accounts for Babies idea were adopted by bank marketing around the country, often in the form of premium schemes whereby retail store customers earned certificates with different face values, corresponding to the amounts of their purchases, which local banks would then accept as if they were cash deposits into children’s accounts. In contrast, Huhn’s $1.00 checks seemed like a superior twist since they went stale after one month and thus wouldn’t create an overhang of liability for the bank.

In addition to targeting newborns, the bank pursued a number of other marketing appeals under Huhn’s leadership. It created a Garden Seed Club for young adults who, in exchange for establishing new accounts with a minimum $1.00 deposit, would receive free packets of garden seeds. It offered free tickets to the state fair to new depositors. The bank sponsored prizes and awarded medals for livestock exhibitions and athletic contests. On an ongoing basis, it used the capacious lobby in its building to run exhibitions showcasing the products, agricultural and industrial, that were evidence of the economic achievements of Louisville. Though not necessarily connected to banking services, the use of its facilities in this way drummed up foot traffic and made the bank a focal point of community engagement and civic pride.

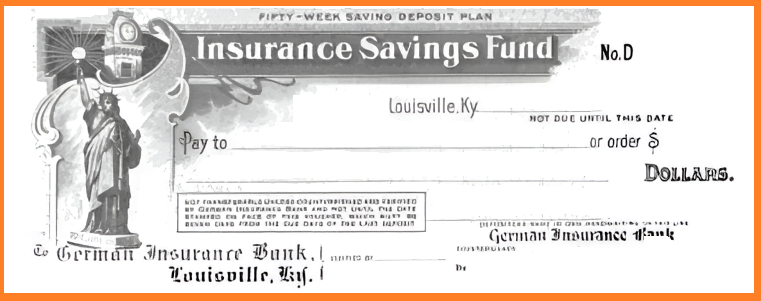

Huhn also developed a term savings plan for his bank’s customers that featured a novel, quasi-compulsory feature. Under the bank’s plan, participating depositors committed to adding funds at predetermined intervals to an “Insurance Savings Fund,” receiving a lump-sum payout, including interest, at the end of the savings plan term, which was set at 50 weeks. Modeled on premium schedules that purchasers of insurance would pay to keep their policies active, the Insurance Saving Fund plan imposed upon savers the discipline of a deposit schedule. Savers could choose from several schedules, starting with weekly contributions as low as 25 cents a week that would, after 50 weeks, result in a payout that a customer could either devote to a planned expenditure or roll over into a new savings plan. Administratively simpler for the bank than managing a bunch of small pass book accounts, Huhn’s scheme was a much more realistic approach to the promotion of saving than simply proclaiming the virtues of thrift. Much of the public discourse surrounding thrift in the early 20th century was tediously hortatory, dwelling on the presumed morality of thrift and its salutary impact upon character. In contrast, Huhn had a more pragmatic appreciation of how savings habits could be built around a rational schedule for satisfying wants.

Facsimile of a draft payable to a participant in Huhn's Insurance Savings Fund. Savers deposited standard amounts at weekly intervals, receiving back their balance, plus interest, after fifty weeks (Image source: The Financier, New York, November 11, 1916).

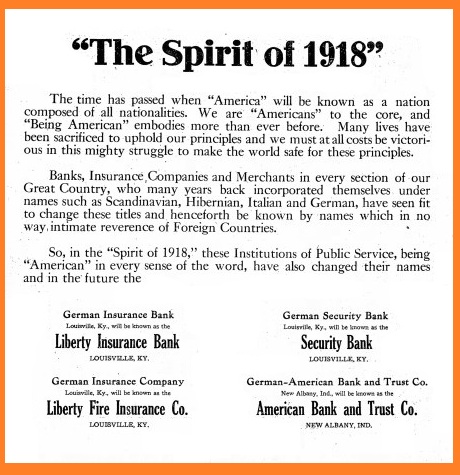

By May 1917, the need to finance the nation’s entry into the European war conscripted financial institutions across the country into the sale of Liberty Bonds. Member banks of the Federal Reserve System, including the German Insurance Bank, were required to participate. All Louisville banks did their part, knowing that public investments in those government securities competed with their own campaigns to increase deposits. The passions unleashed by the war also forced name changes to any financial institution associated with Germany. For Louisville, with a large German population since the 1850s, this had to have been an unpleasant experience. In March of 1918, four local financial institutions with “German” in their names were duly rechristened, the German Insurance Bank becoming “Liberty Insurance Bank”, and its insurance twin “Liberty Fire Insurance.” In a newspaper announcement published by all four institutions, the moment was heralded as the “Spirit of 1918,” reflecting a more assertive, war-fueled American nationalism. Businesses across the country which “many years back incorporated themselves under names such as Scandinavian, Hibernian, Italian, and German, have seen fit to change their titles and henceforth be known by names which in no way intimate reverence of Foreign Countries.” Including those other traditions in the banks' announcement perhaps softened the blow, but the reality was that German identity represented the real target.

Four Louisville-area banks proclaimed their American-ness by expunging "German" from their names (Image source: The Courier-Journal, Louisville, KY, March 3, 1918).

Louisville’s School Savings Program

The savings initiative that Huhn was most known for, Louisville’s school savings program, was not one that immediately expanded his bank’s deposit base but which served the broader agenda of thrift promotion. In early 1916 Huhn began working with a sympathetic school principal at the Second Ward School to create a scheme where students could start savings accounts with as little as one cent, after which students could deposit whatever spare change they had, competing to see whose balances were higher. While the accounts would be administered through the school, the numerous tiny contributions made by students would be aggregated into a single deposit with the German Insurance Bank that paid the students 3% interest.

The school savings idea didn’t originate with Huhn. Indeed, similar schemes were multiplying across the country as part of the thrift movement. A New York based outfit, Educational Thrift Service Inc., had created an organizational template for student savings banks that it promoted for adoption nationwide. With the permission of Louisville school officials, Huhn invited the Service to administer school savings programs in other Louisville schools, and by 1920 Huhn’s bank (by now renamed the Liberty Insurance Bank) served as the sole depository for some $40,000 in student deposits from across the city. Some of these student deposits had grown large enough that they could be rolled over into the purchase of Liberty Bonds, which linked the virtues of juvenile thrift to the patriotic mobilization on behalf of the war effort.

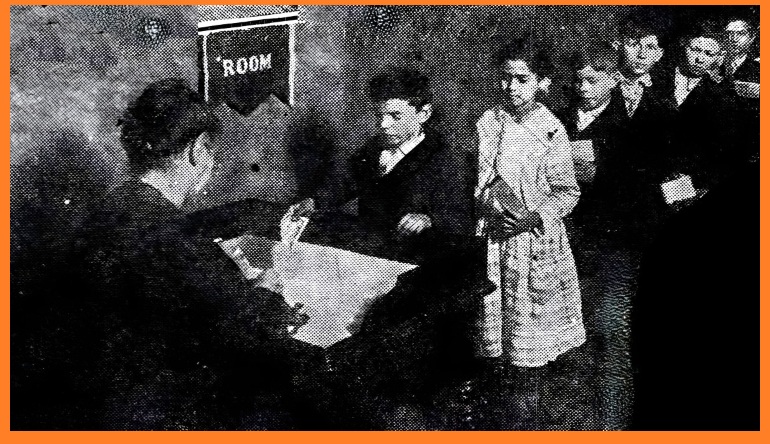

Under the Educational Thrift Service’s plan, Louisville schools hosted “bank day” once a week, when students paraded up to offer their meager funds for deposit. The amount that had accumulated in the Liberty Bank’s coffers was tiny compared with its overall deposits, but those student accounts did represent a much larger number of future potential depositors, and thus a marketing advantage which the Liberty Bank exploited and which other banks resented. In 1920, the Louisville Clearing House Association called for those student deposits to be prorated amongst its members, and by 1923 fourteen Louisville banks supplanted Liberty Bank’s monopoly by creating the Louisville School Thrift Council to supervise the program. The following year, thirty thousand students across the city from high school on down had deposited over $153,000, a 54% participation rate. As impressive as this growth in deposits was, Louisville banks acknowledged that there was no direct profit to be had from sustaining the student savings program. Instead, between their own costs and what they paid Educational Thrift Service to run the program, the banks were taking a loss which they accepted as a public service, or at least a marketing expense for the sake of the future business that might come their way from thrift-conscious students.

Students line up to make deposits to their school savings accounts on "bank day" at the Upper Fulton School in Louisville, Kentucky (Image source: The Courier-Journal, Louisville, KY, April 6, 1924).

Meanwhile, Liberty Insurance Bank continued its own efforts to attract deposits, particularly the Bank Accounts for Babies plan, which no other bank in Louisville seems to have imitated. After having sold so many Liberty Bonds to Louisvillians during the war, the bank then pivoted to offering free custodial services to those bondholders, in the hopes that their dividend payments might add to the bank’s deposit base. Likewise, when Congress passed the Adjusted Compensation Act of 1924, conferring “Adjustment Compensation Certificates” upon military veterans to make up for the civilian wages they had foregone by wartime service, the Liberty Bank created a free safekeeping program for certificate holders. Unlike Liberty Bonds, which produced regular dividends, what was widely known as the “Soldier’s Bonus” wouldn’t become payable until 1945. Still, as they sat secure in the bank’s vaults, those certificates could serve as good collateral for any future loans which the bank would be happy to make to their owners. Finally, in addition to all its other savings incentives, the Liberty Bank took advantage of new technologies. By the late 1920s, as radio quickly grew to become a form of mass entertainment, Liberty regularly sponsored radio broadcasts whose content had some thrift angle.

In 1927, John E. Huhn assumed the Presidencies of both the Liberty Insurance Bank and the Liberty Fire Insurance Co. This achievement seemed like a fitting capstone to a career that had begun some thirty years earlier as a lowly runner in the same institution. As President, Huhn diversified the bank’s services by creating a trust department (thus warranting another name change, to Liberty Bank & Trust Co., in 1928). He also expanded its branch network and increased the bank’s real estate loan portfolio. The onset of the Great Depression took the wind out of the thrift movement in Louisville and across the United States, as the public had less appetite for promoting the habit of saving and a greater concern for the basic solvency of their banks. As the historian Andrew L. Yarrow put it, "exhortations to save money may have seemed grotesquely out of touch in a country with at least 25 percent unemployment, banks failing, and the savings of millions of people wiped out."

Unfortunately for him, the Great Depression also seemed to put a quick end to Huhn's corporate career. In January 1934 he stepped down from the bank presidency in favor of Merle E. Robertson, a thirty-three year old financial wunderkind from New Jersey who had joined the bank only two years earlier. Huhn continued as head of the insurance company only briefly, resigning in October that same year. Under Robertson, the bank adopted a national charter the following year that made it eligible for a capital injection from the Reconstruction Finance Corporation, allowing the bank to write off bad real estate loans and emerge from the Depression with a stronger balance sheet. It continued operating as the Liberty National Bank and Trust Co. for the next sixty years until 1995, when it changed its name to Bank One and went on a brief acquisition spree. A decade later it was in turn absorbed by J.P. Morgan Chase.

Samuel Wilkes, Jr.: The Boy Who Never Saw His First Dollar, but Lived.

The $1.00 check pictured above exists only because the parents of the child for whom it was intended never created the bank account. But who was this unfortunate creature deprived of their financial birthright? The question can be answered by beginning with the same research that led to the sending of the letter to begin with—consulting the birth notices in the Louisville newspaper. And lo, according to The Courier-Journal of November 25, 1924, unto Samuel and Sarah Wilkes of 1606 Rosewood Ave, a child was born, indeed a male, on November 12, inst. The 1930 Census reveals his name as Samuel O. Wilkes, Jr., younger brother to John Wilkes.

Despite his impecunious beginnings, young Samuel managed to grow up and have a life. By 1940, Wilkes Senior had moved his family to Huntington, West Virginia, where he worked in his father’s restaurant supply business until the father’s death in 1946. At age 18, according to his WWII draft card, Samuel Ouerbacker Wilkes, Jr. was enrolled at Marshall College in Huntington. In the late 1940s Samuel married Estella Farr (b. 1925), who attended the same Huntington high school as he did. Details about his subsequent employment history are sparse. In 1953 his Korean War draft card placed him as a shipping clerk for the Graybar Electric Co. in Louisville. That same year Samuel and Estella relocated to Jacksonville, Florida, possibly following Samuel’s older brother, John, who had started a restaurant supply business there similar to the one his grandfather operated back in Huntington. In Florida, Estella became active as a real estate agent. There in Jacksonville, Samuel O. Wilkes, Jr., the boy who never saw his first dollar, passed away in 1995.

.................

REFERENCES

Ancestry.com, for basic biographical information about the Samuel Wilkes family.

The Bankers Magazine (March 1927), p. 512 (Huhn becomes bank President, with picture).

The Courier-Journal, Louisville, KY, March 18, 1916; May 3, 1916; June 6, 1917; March 3, 1918; January 18, 1920; February 22, 1920; July 18, 1920; September 12, 1923; April 6, 1924; November 25, 1924; January 2, 1934; October 17, 1934; January 9, 1935.

(Huhn's obituary in The Courier-Journal, September 19, 1968, incorrectly states that he continued as President of both the bank and the insurance company until 1950. Newspaper references from 1934 onward clearly show that he left both positions, worked for a time as an independent insurance broker, and otherwise faded from public life.)

“If it’s Good, Put it in the Lobby” The Burroughs Clearing House (November 1920), pp. 12-14, 23.

Millican, W. A. “Safekeeping for the Soldier’s Bonus” The Burroughs Clearing House (April 1925), p. 26.

Murphy, Carobel, Thrift Through Education (NY: A. S. Barnes and Co. 1929), pp. 15, 114-117 (about the Educational Thrift Service).

"New Savings Fund Plan" The Financier, New York, November 11, 1916, pp. 1305, 1314-15,

Riebel, Raymond Charles, Louisville Panorama: A Visual History of Louisville (Liberty National Bank & Trust Co., 1954), p. 210 (profile of John E. Huhn).

"Savings Accounts and Gardens" The Financier, New York, April 21, 1917, p. 1033.

Sutch, Richard, “Liberty Bonds, April 1917-September 1918” Federal Reserve History. Accessed at:

https://www.federalreservehistory.org/essays/liberty-bonds

Ulrich, Robert and Victoria A., German Influences in Louisville (Arcadia Publishing, 2019), pp. 39-40.

Yarrow, Andrew L., Thrift. The History of an American Cultural Movement (University of Massachusetts Press, 2014), ch. 4 (about school savings plans); "exhortations to save money" quote p. 126.